The Pension System in the United Kingdom : A Model of Retirement Security and Lessons for India

By Lokanath Mishra

Introduction

During my recent visit to London, I had the opportunity to meet and interact with several elderly citizens. What impressed me most was their sense of security, independence, and satisfaction with life. Most pensioners appeared financially comfortable and free from the anxieties that often accompany old age. Their happiness was not merely the result of personal wealth but was supported by a comprehensive pension and social welfare system developed over many decades.

This experience inspired me to examine the pension system of the United Kingdom and compare it with that of India. Such a comparison provides valuable insights into how different societies care for their senior citizens and what lessons India may learn as its elderly population continues to grow.

The Foundation of the British Pension System

The British pension system is based on the principle that citizens who contribute to society during their working lives should receive financial support in retirement. Workers pay National Insurance contributions throughout their careers, and these contributions help finance the State Pension.

To qualify for the full State Pension, a person generally needs around thirty-five years of National Insurance contributions. Those with fewer years may still receive a partial pension, provided they have a minimum qualifying record.

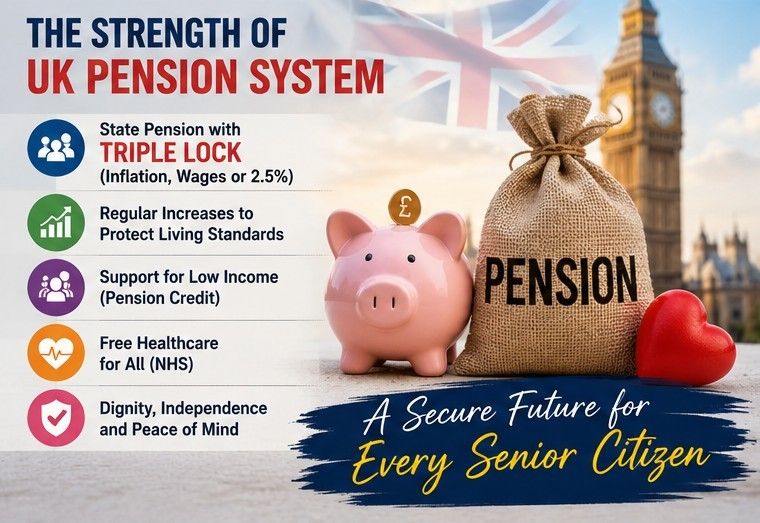

One of the most remarkable features of the British system is the “Triple Lock” guarantee. Under this arrangement, the State Pension rises every year by whichever is highest among inflation, average wage growth, or 2.5 percent. This mechanism protects pensioners from rising living costs and allows them to share in the country’s economic progress.

In April 2026, the British government increased the State Pension by 4.8 percent. The full New State Pension reached approximately £241 per week, or more than £12,500 annually. This increase provided pensioners with roughly £575 of additional income each year. More than twelve million pensioners benefited from this rise.

Additional Benefits Beyond the State Pension

The State Pension is only one component of retirement security in Britain. Pensioners may also receive a range of other benefits depending on their income and circumstances.

Those with low incomes can receive Pension Credit, which supplements their weekly earnings and helps them maintain a minimum standard of living. Pension Credit also opens the door to additional support, including assistance with housing costs and council tax reductions.

Healthcare is another major benefit. Through the National Health Service (NHS), elderly citizens have access to medical consultations, hospital treatment, emergency care, and many other health services without direct charges at the point of use. This significantly reduces the financial burden associated with ageing.

Many local authorities also provide concessions for public transport. Elderly citizens often travel free on buses and receive discounts on other forms of transportation. Various schemes also help pensioners cope with winter heating expenses, an important consideration in Britain’s cold climate.

Together, these benefits create a strong social safety net that helps older citizens maintain their dignity and independence.

Retirement Benefits for Government Employees in the United Kingdom

Government employees in the United Kingdom generally enjoy retirement benefits that are considerably more generous than those available to many private-sector workers.

Civil servants, teachers, members of the armed forces, police officers, firefighters, National Health Service employees, and local government workers participate in occupational pension schemes sponsored by the government.

These occupational pensions are separate from the State Pension. As a result, retired government employees usually receive two streams of retirement income.

The first is the State Pension, which is available to all eligible citizens who have made sufficient National Insurance contributions.

The second is an occupational pension earned through government service. Depending on length of service, salary history, and the specific pension scheme, this occupational pension can be substantial.

For example, a retired teacher, nurse, civil servant, or police officer may receive several thousand pounds annually in addition to the State Pension. In many cases, the occupational pension may exceed the State Pension itself.

Most government pension schemes are indexed to inflation. This means that pension payments are increased periodically to protect retirees from rising living costs. Consequently, retired public servants often enjoy stable incomes throughout their retirement years.

Another significant advantage is survivor protection. If a retired government employee dies, a spouse or dependent may continue receiving a portion of the pension. This provides long-term financial security for families.

Many retired public servants also benefit from lump-sum payments at retirement, depending on the rules of their particular scheme. These payments can help clear debts, improve housing conditions, or provide a financial reserve for old age.

As a result of these arrangements, many retired government employees in Britain enjoy comfortable and secure retirements. It is common to find retired teachers, nurses, engineers, military officers, and civil servants maintaining an active lifestyle well into their later years.

The Indian Pension System

India’s pension structure differs significantly from that of the United Kingdom.

Government employees in India traditionally enjoyed defined-benefit pensions, although newer recruits are generally covered under the National Pension System (NPS) or UPS. Pension benefits therefore vary depending on the date of appointment and service conditions.

Workers in the organized private sector may receive retirement benefits through the Employees’ Provident Fund and Employees’ Pension Scheme. However, the pension component is often modest and may not provide sufficient income after retirement.

For millions of workers in the informal sector, retirement security remains a challenge. Many rely on personal savings, family support, or government welfare programmes. Old-age pensions provided under central and state welfare schemes are valuable but often relatively small compared with living expenses.

The National Pension System has expanded retirement savings opportunities, but participation remains far below the level seen in many developed countries.

Comparing the United Kingdom and India

The difference between the two systems is striking.

In Britain, retirement income is viewed as a social right earned through contributions and citizenship. The State Pension provides a strong financial foundation, and many retirees receive additional occupational pensions from their employers. Pension increases are protected through the Triple Lock mechanism, ensuring that incomes generally keep pace with inflation and wage growth. Healthcare is largely free through the NHS, and numerous supplementary benefits are available for those with lower incomes.

In India, pension coverage is much more uneven. Government employees often receive relatively good retirement benefits, but large sections of the population, particularly those working in the informal sector, have limited pension protection. Inflation-linked pension increases are not universally available, and many elderly citizens remain dependent on family support. Healthcare expenses can also become a significant financial burden during retirement.

Consequently, the average British pensioner enjoys a higher level of economic security than the average Indian pensioner. This difference becomes particularly visible in daily life. Elderly people in Britain are often able to live independently, travel, participate in community activities, and maintain a comfortable standard of living without relying heavily on their children.

Challenges Facing the British System

Despite its success, the British pension system faces important challenges. The country’s ageing population means that a growing number of retirees must be supported by a relatively smaller working population. Pension expenditures continue to rise, and some economists question whether the Triple Lock policy can be sustained indefinitely.

Nevertheless, there remains broad public support for protecting pensioners, and successive governments have continued to prioritise retirement security.

Lessons for India

India can learn several important lessons from the British experience.

First, pension coverage should be expanded so that all citizens, including informal-sector workers, have access to retirement income security.

Second, pension benefits should be regularly adjusted to protect against inflation.

Third, occupational pension schemes should be strengthened and encouraged across both public and private sectors.

Fourth, healthcare support for senior citizens should be expanded to reduce the burden of medical expenses in old age.

Finally, retirement planning and long-term savings should become an integral part of financial education for all workers.

Conclusion

The happiness and confidence I observed among British pensioners are the result of a carefully designed system that combines State Pensions, occupational pensions, healthcare services, and social welfare benefits. Retired government employees enjoy particularly strong protection through generous occupational pension schemes that supplement the State Pension and provide long-term financial stability.

India has made notable progress in pension reform, but much remains to be done. As the nation moves toward becoming one of the world’s largest ageing societies, the challenge of ensuring dignity and security in old age will become increasingly important. A stronger and more inclusive pension system, inspired by successful international models such as that of the United Kingdom, could greatly improve the quality of life of millions of Indian senior citizens.

The true measure of a civilized society is how it treats its elderly. In this respect, the British pension system offers valuable lessons for India as it prepares for the demographic realities of the twenty-first century.