Human Resource Management and Employees’ Associations in India’s Revenue Administration: A Critical Comparative Study of CBDT and CBIC

By Lokanath Mishra, MA, LLB, IRS ( retired)

The Department of Revenue under the Ministry of Finance, Government of India, occupies a pivotal position in the country’s economic governance. Through the collection of direct and indirect taxes, it mobilizes the financial resources required for national development, infrastructure, defence, social welfare, healthcare, education, and economic growth. This immense responsibility is discharged through two premier organizations—the Central Board of Direct Taxes (CBDT) and the Central Board of Indirect Taxes and Customs (CBIC).

Although both Boards function under the same Ministry and are expected to uphold identical standards of administrative excellence, fairness, and employee welfare, their organizational culture, human resource management practices, career progression systems, and employee association movements have evolved in remarkably different ways. These differences have significantly influenced employee morale, organizational unity, industrial relations, and administrative efficiency.

This article critically examines these contrasting organizational models and argues that unless CBIC undertakes comprehensive reforms in human resource management, cadre administration, promotional policies, and employee representation, its long-term institutional effectiveness and workforce morale may continue to be adversely affected.

The Department of Revenue is one of the most strategically important departments of the Government of India. It is entrusted with framing tax policies, administering taxation laws, combating tax evasion, facilitating legitimate trade, preventing smuggling, and safeguarding the nation’s financial interests.

Its responsibilities are discharged through two statutory Boards:

- Central Board of Direct Taxes (CBDT)

- Central Board of Indirect Taxes and Customs (CBIC)

Both organizations are pillars of India’s fiscal administration. Yet, despite functioning under the same Ministry, they present two entirely different models of human resource development and employee participation.

The contrast is so striking that it offers valuable lessons in organizational behaviour, employee motivation, leadership, and institutional governance.

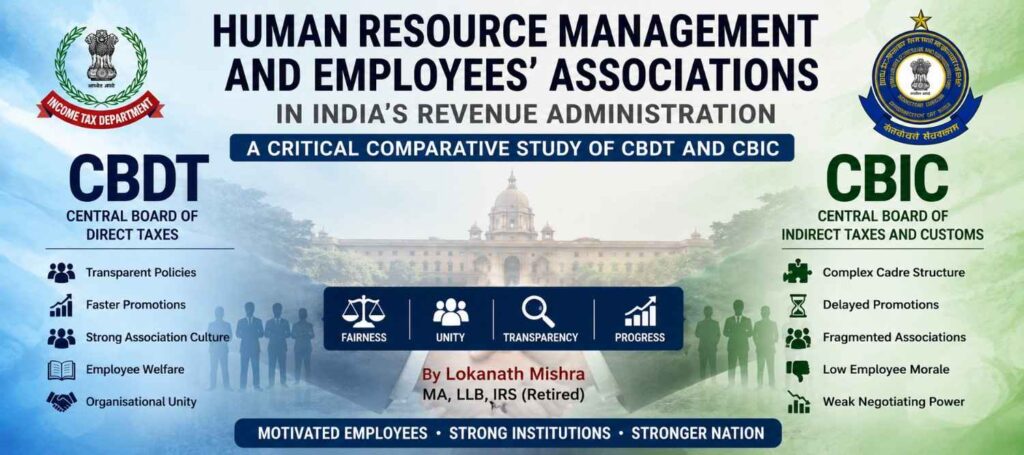

Human Resource Management in CBDT: A Model of Institutional Stability:

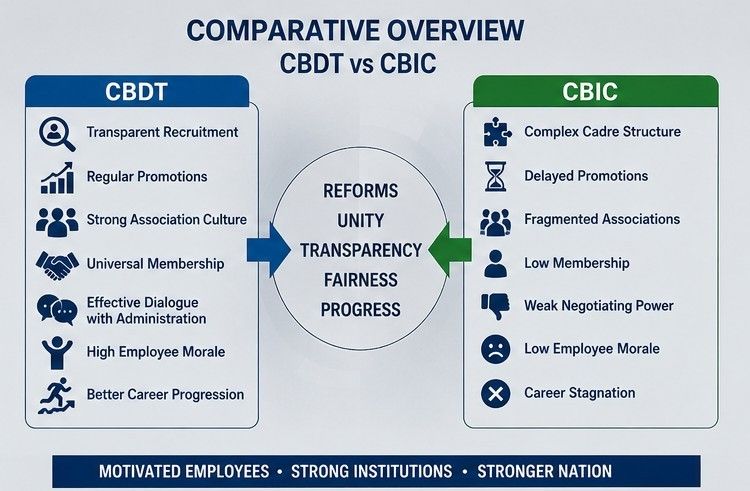

CBDT has, over several decades, evolved into an organization where human resource management occupies a central place in administrative planning. The Board has consistently recognized that an efficient tax administration depends not merely on technology or legislation but on a motivated, professionally satisfied, and career-oriented workforce.

Its HR policies are comparatively systematic, transparent, and employee-centric.

Among the important features are:

- well-defined recruitment rules;

- transparent promotional policies;

- departmental examinations providing equal opportunities for advancement;

- comparatively faster career progression in many cadres;

- structured manpower planning;

- continuous training and skill development;

- systematic cadre management;

- effective interaction between the administration and recognized employee associations.

Such a framework creates confidence among employees that professional competence, experience, and merit will receive due recognition.

This confidence generates commitment, organizational loyalty, and a strong sense of belonging, enabling employees to devote themselves wholeheartedly to the institution.

CBDT’s Strong Association Culture: The Foundation of Collective Strength:

Perhaps the greatest strength of CBDT lies in its vibrant and disciplined association movement.

The overwhelming majority of officers and employees actively participate in their service associations. Membership is regarded not merely as an option but as a collective responsibility towards safeguarding service conditions and strengthening the organization.

These associations are characterized by:

- almost universal membership;

- regular collection of subscriptions;

- democratic functioning;

- disciplined organizational structure;

- accountability to members;

- affiliation with national federations and confederations;

- continuous dialogue with the Government;

- effective collective bargaining.

Most importantly, these associations possess considerable negotiating strength because they represent an overwhelmingly united workforce.

Whenever important service matters arise, the administration recognizes that these associations speak with one voice. Their bargaining power stems from unity, organizational discipline, credibility, and the confidence reposed in them by their members. They are capable of adopting democratic organizational measures—including peaceful demonstrations, non-cooperation programmes, and, where legally permissible, strike notices—to ensure that legitimate employee grievances receive serious consideration.

Consequently, issues relating to promotions, cadre restructuring, pay anomalies, transfers, service conditions, and employee welfare often receive timely attention.

Their success demonstrates a timeless principle: unity is the greatest strength of any employees’ movement.

CBIC: An Institution Rich in Talent but Confronted with Organizational Fragmentation:

CBIC is among the largest and most complex revenue organizations in India. It administers Customs, GST, Central Excise legacy matters, anti-smuggling operations, narcotics control, trade facilitation, and several other strategically important functions.

Despite its enormous responsibilities and the exceptional competence of its workforce, the organizational climate relating to human resource management presents several longstanding challenges.

Unlike CBDT, employee representation in CBIC has remained fragmented.

Instead of one cohesive movement representing the collective interests of employees, there exist numerous All India Associations representing different cadres and services. In several cadres, more than one association claims to represent the same employees, leading to division of strength, duplication of efforts, and weakened bargaining capacity.

Many employees perceive that organizational divisions have sometimes arisen because of differences in leadership approaches, cadre interests, or personal ambitions. Whatever the reasons, the result has often been a fragmented voice before the Government.

A divided workforce can rarely negotiate as effectively as a united one.

History repeatedly demonstrates that organizational fragmentation invariably weakens collective bargaining.

Persistent Cadre Imbalances and Promotional Disparities:

One of the most frequently discussed concerns within CBIC relates to disparities in promotional opportunities among different cadres.

Many employees perceive that certain cadres—particularly Examiner and Appraiser streams—have historically enjoyed comparatively faster career progression because of recruitment patterns, cadre restructuring, organizational priorities, or service rules.

Employees belonging to the Central Excise executive formations often express concerns regarding:

- limited promotional avenues;

- prolonged stagnation;

- uneven career progression;

- regional disparities in promotions;

- delays in cadre restructuring;

- unfilled vacancies;

- prolonged service grievances;

- absence of comprehensive measures to remove inter-cadre and intra-cadre disparities.

Whether every perception is fully justified or not, these issues have undoubtedly influenced employee morale and created a widespread demand for greater transparency and equity in career management.

An organization can achieve lasting harmony only when every employee believes that promotional opportunities are governed by fairness, objectivity, and equal treatment rather than historical imbalances.

Weakening Association Participation: A Matter of Serious Concern:

Perhaps the greatest challenge facing employee organizations in CBIC is the declining culture of collective participation.

Many employees understandably focus on their individual careers, transfers, postings, promotions, or personal service matters. However, comparatively fewer employees actively participate in strengthening their associations.

This situation has several consequences:

- declining membership;

- inadequate financial resources;

- weakened organizational activities;

- reduced bargaining strength;

- limited support for elected leadership;

- erosion of collective unity.

Employees also express concern that organizational divisions occasionally deepen because competing groups seek separate platforms instead of strengthening existing representative bodies. Such fragmentation, irrespective of the motivations behind it, weakens the collective voice of employees.

An association cannot become strong merely because it has capable office-bearers.

Its real strength lies in the commitment, participation, financial support, and unity of its members.

Historical Legacy and Its Continuing Impact:

The present situation cannot be understood without examining the historical evolution of Central Excise administration.

During the era of Physical Control and later under the Production Based Control (PBC) system, promotional opportunities for many executive officers were comparatively limited. Many officials preferred to remain in field formations rather than accept transfers associated with higher responsibilities.

These historical realities shaped organizational attitudes over several decades.

However, the introduction of RBC , then GST has fundamentally transformed indirect tax administration.

Today’s environment demands:

- digital governance;

- national mobility;

- technological competence;

- continuous learning;

- specialized professional knowledge;

- integrated cadre management;

- transparent career planning.

Accordingly, both administrative policies and employee attitudes must evolve to meet the demands of a modern tax administration.

Collective Responsibility: The Only Sustainable Solution:

Every employee legitimately expects:

- timely promotions;

- transparent transfer policies;

- equal career opportunities;

- fair cadre management;

- recognition of merit;

- protection of service rights;

- dignity and respect in public service.

However, these objectives cannot be secured by a handful of association leaders alone.

Every employee has a moral responsibility to strengthen the collective institution by:

- becoming an active member;

- paying subscriptions regularly;

- participating in meetings;

- contributing constructive ideas;

- supporting democratic leadership;

- avoiding unnecessary organizational divisions;

- placing institutional interests above personal considerations.

Strong associations are not built by speeches; they are built by active participation.

Lessons CBIC Can Learn from CBDT:

CBDT offers several valuable lessons worthy of careful consideration.

CBIC should consider:

- Formulating a comprehensive Human Resource Management Policy.

- Establishing transparent and equitable promotional systems.

- Removing inter-cadre and intra-cadre disparities through objective cadre review.

- Strengthening manpower planning.

- Encouraging wider employee participation in representative associations.

- Building organizational unity across cadres.

- Institutionalizing regular consultations with employee representatives.

- Developing long-term leadership capable of representing employees with credibility and unity.

These reforms are essential not only for employee welfare but also for enhancing administrative efficiency and institutional stability.

The Way Forward:

India’s revenue administration is entering an era of unprecedented complexity.

Artificial intelligence, digital taxation, global commerce, data analytics, cyber-enabled financial crimes, international trade agreements, and evolving GST architecture require an exceptionally skilled, motivated, and united workforce.

The greatest asset of both CBDT and CBIC is not technology, legislation, or infrastructure—it is their human resources.

An organization divided by cadre rivalries, fragmented representation, and unequal opportunities cannot fully realize its potential.

Conversely, an organization founded upon fairness, transparency, unity, professionalism, and participative leadership becomes capable of meeting every administrative challenge.

Conclusion:

CBDT and CBIC constitute the twin pillars of India’s revenue administration. Yet their experiences clearly demonstrate that institutional success depends not merely upon statutory powers or administrative authority, but upon the quality of human resource management and the strength of employee participation.

CBDT has demonstrated how structured HR policies, transparent career progression, and a united association movement can foster confidence, organizational stability, and effective collective bargaining.

CBIC, while possessing immense professional talent and performing some of the most demanding responsibilities in the Government of India, continues to face important challenges relating to cadre disparities, fragmented employee representation, uneven promotional opportunities, and limited collective participation.

The time has come for a comprehensive review of human resource policies, cadre management, promotional systems, and employee relations. Reforms should be guided by the principles of equity, transparency, accountability, and organizational unity rather than by historical precedents or sectional interests.

Ultimately, no organization can become truly strong if its employees remain divided. Rules may create an institution, but unity creates strength. Human resource management may govern careers, but trust governs commitment. Employee associations may represent grievances, but only collective participation can transform them into powerful instruments of constructive change.

A united workforce, equitable human resource policies, transparent promotions, and strong democratic employee associations are not merely desirable—they are indispensable prerequisites for building a modern, efficient, and responsive revenue administration worthy of serving the aspirations of a rapidly developing India.