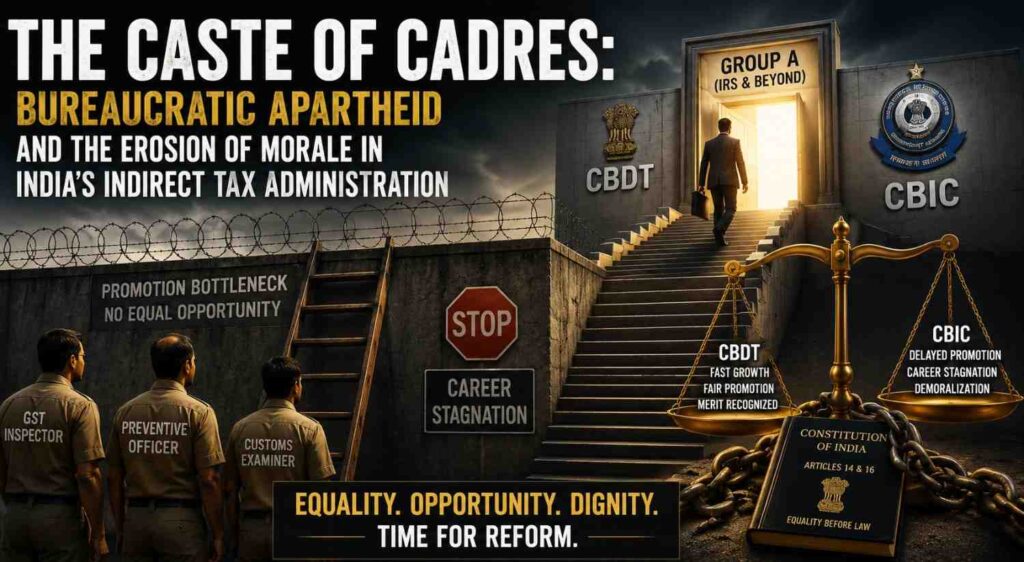

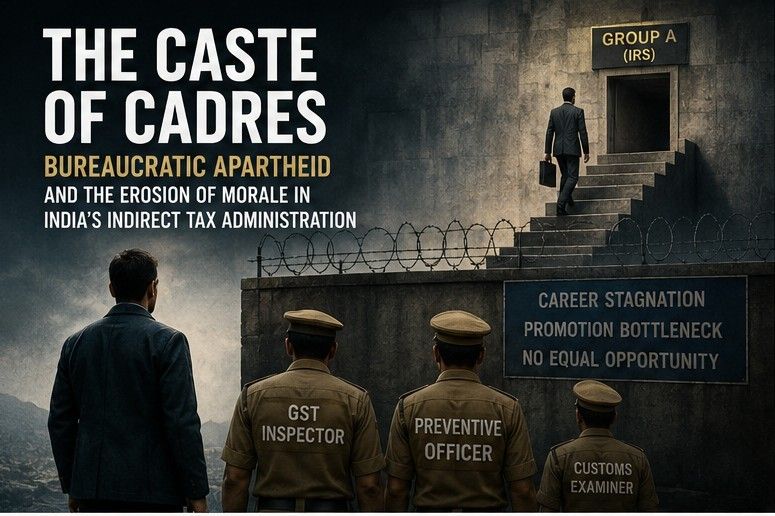

THE CASTE OF CADRES : BUREAUCRATIC APARTHEID AND THE EROSION OF MORALE IN INDIA’S INDIRECT TAX ADMINISTRATION

Lokanath Mishra, MA, LLB, IRS ( retired)

ABSTRACT

While the Central Board of Direct Taxes (CBDT) has institutionalized structured and time-bound career progression for its personnel, the Central Board of Indirect Taxes and Customs (CBIC), its counterpart under the Department of Revenue, functions as a structural barrier to the aspirations of its non-Group A executive cadre. This paper argues that CBIC’s promotion architecture constitutes a form of “bureaucratic apartheid” — a rigid, anachronistic hierarchy that condemns thousands of GST Inspectors, Preventive Officers, and Examiners to professional stagnation. The article examines the institutional causes of this stagnation and proposes a legally and politically coordinated response to restore equity, efficiency, and dignity to the cadre.

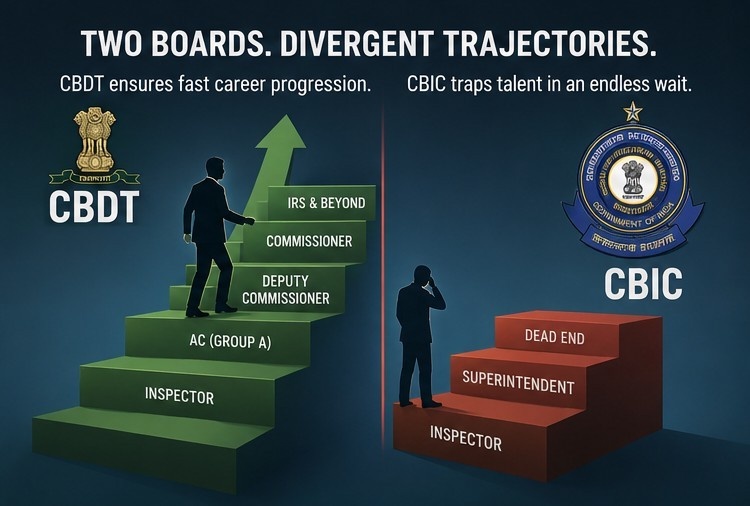

- INTRODUCTION: TWO BOARDS, DIVERGENT TRAJECTORIES

Both CBDT and CBIC operate under the Department of Revenue, Ministry of Finance, and are entrusted with the critical function of revenue mobilization for the Indian State. Yet their human resource policies reflect diametrically opposite philosophies.

CBDT has, through successive cadre restructurings, ensured relatively fast, predictable, and merit-based progression from Inspector to senior IRS grades. CBIC, formerly CBEC, has instead acquired a reputation as an institutional “graveyard” for its Group B executive officers.

For thousands who enter CBIC through the Staff Selection Commission, the initial promise of public service collapses into a decades-long career freeze. A system that ought to reward competence and experience has instead calcified into a steep, exclusionary pyramid.

- THE BOTTLENECK: THREE STREAMS, ONE IMPASSE

The CBIC Group B executive cadre is recruited through three distinct SSC channels: - Examiners: Responsible for customs appraisal. Traditionally the fastest stream, yet still subject to promotion delays of 10-12 years.

- Preventive Officers: Tasked with customs enforcement, anti-smuggling, and port/airport vigilance.

- GST/Central Excise Inspectors: The largest stream, handling assessment, audit, investigation, and taxpayer administration under GST and erstwhile Central Excise.

At the base, the volume of recruitment is substantial. However, upon reaching the grade of Superintendent, officers encounter an absolute glass ceiling. Promotion from Inspector to Superintendent routinely takes 15-20 years in several zones. Promotion beyond Superintendent to Group A as Assistant Commissioner is statistically insignificant due to UPSC-dominated direct recruitment quotas.

Consequently, officers with 25-30 years of domain expertise retire in the same functional grade in which they began, while discharging responsibilities that far exceed their pay, rank, and promotional prospects.

- THE INSTITUTIONAL COST OF STAGNATION

This is not merely a grievance of service conditions. The structural stagnation has cascading consequences: - Morale Collapse: A permanent underclass of experienced officers breeds resentment, disengagement, and attrition of talent.

- Administrative Inefficiency: Critical policy implementation under GST is executed by officers denied decision-making authority commensurate with their experience.

- Comparative Inequity: CBDT counterparts with identical entry qualifications attain IRS and higher administrative grades within 12-15 years. The disparity violates the principle of equal opportunity under Article 16 of the Constitution.

- Governance Risk: A juniorized, demotivated field force cannot provide the institutional feedback or leadership required for a tax system as complex and dynamic as GST.

By preserving a monopoly of Group A entry for one service, the department has institutionalized a two-tier bureaucracy: one for policy-makers, and another for those who implement policy.

- A BLUEPRINT FOR REFORM: THE CASE FOR AN ALL-INDIA CADRE MOVEMENT

This systemic injustice cannot be remedied through passive compliance or isolated representations. The administrative apparatus has demonstrated no willingness to voluntarily cede privilege. What is required is a coordinated, assertive, and legally grounded All-India Cadre Movement led jointly by the associations of GST Inspectors, Preventive Officers, and Examiners.

The campaign must proceed on three strategic fronts:

4.1 The Legal Offensive: Challenging Discriminatory Recruitment Rules

A consolidated challenge must be mounted before the Central Administrative Tribunal and the Hon’ble Supreme Court against the skewed direct-recruit to promotee ratios in CBIC Recruitment Rules.

Legal Ground: Violation of Article 14 – Right to Equality, and Article 16 – Equality of Opportunity in Public Employment.

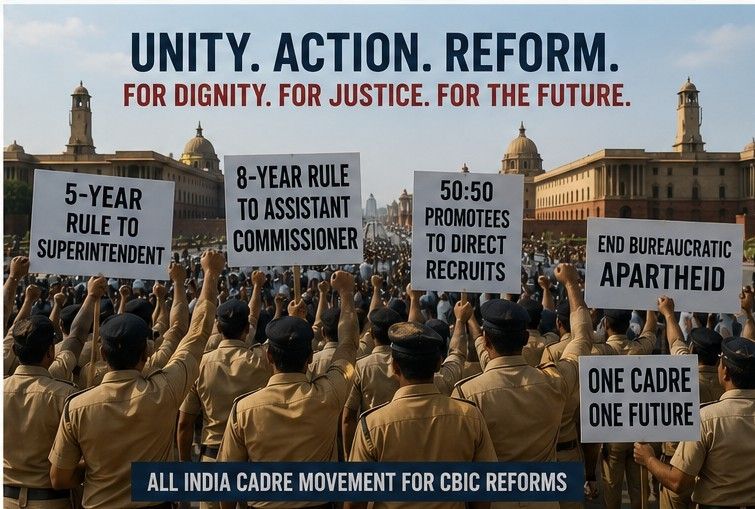

Core Demand: Statutory parity with CBDT in promotion timelines and quotas. Judicial mandate for a minimum 50:50 ratio between UPSC direct recruits and departmental promotees at the entry level of Group A.

4.2 Radical Policy Advocacy: The Time-Bound Promotion Framework

The movement must demand assured career progression delinked from artificial vacancy constraints:

- 5-Year Rule: Automatic promotion of any GST Inspector to Superintendent upon completion of 5 years of service.

- 8-Year Rule: Automatic promotion of any Superintendent to Assistant Commissioner after 8 years of service.

- Cadre Restructuring: Creation of an in-service promotion channel to Group A, recognizing domain expertise as equivalent to direct recruitment.

Such a framework will align CBIC with modern public personnel management principles and with the practices already prevailing in CBDT.

4.3 Strategic Leverage: Institutional Non-Cooperation

Ground-level officers constitute the operational backbone of India’s indirect tax machinery. A disciplined “Work-to-Rule” campaign — strict adherence to statutory working hours, withdrawal of unpaid overtime, and cessation of informal facilitation for systemic gaps — will demonstrate the cadre’s indispensability.

If required, coordinated mass casual leave during peak revenue periods, such as the March-end quarter, will compel the Ministry of Finance to engage directly with representative associations.

- CONCLUSION: DISMANTLING BUREAUCRATIC APARTHEID

The administrative paralysis within CBIC is a self-inflicted wound. By treating its most experienced field officers as a permanent subordinate class, the department has fostered a culture of resentment, low morale, and institutional decay.

Individual strategies such as pursuing higher ACR gradings are insufficient remedies for a structurally defective system. The era of polite memoranda has ended.

Only a unified, legally backed, and politically visible All-India movement can compel the political leadership to restructure CBIC, dismantle the monopoly of a single service lobby, and restore basic dignity and career progression to the foot soldiers of India’s tax administration.

Until that occurs, CBIC will continue to collect revenue efficiently for the nation, while systematically demoralizing the very personnel who generate it.